Housing market outcomes are the result of the interaction between user demand and supply of housing. For several years, additional housing demand exceeded additional housing supply leading to exceptional growth in selling prices. However, over the past two years, house prices grew at a slower pace. Thus, understanding the historical and expected developments in the demand and supply of housing is key for anticipating likely developments in the selling price of housing units.

The main drivers of ‘user demand’ for housing stems from first-time buyers, long-term lessees and short-stay visitors. This should not be confused with ‘buyer demand’ which represents those that purchase a housing unit either for personal use or to rent it out.

The additional demand for housing units by first-time buyers remained relatively stable over several years and is estimated to average around 2,500 units per annum.

The demand driven by long-term lessees mainly stems from foreign residents working or retiring in Malta. These increased significantly since 2017 and, by 2019, 100,000 out of a 500,000 population were foreign-born living in Malta. Such was their increase, that additional demand for housing units by long-term lessees is estimated to have amounted to almost three times that of first-time buyers in 2019.

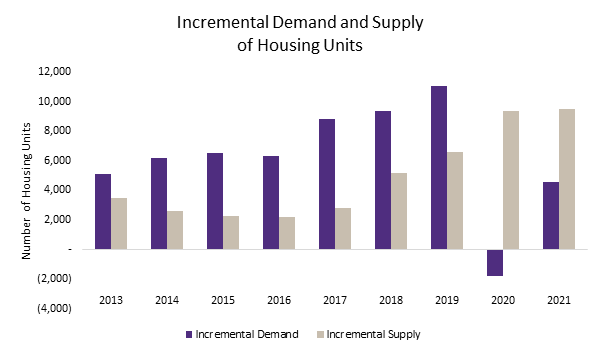

A similar trend is observed for short-stay visitors. These are tourists staying in temporary accommodation that would otherwise serve as housing. Tourism numbers followed the same trend as foreign residents, whereby a total of 714,157 tourists stayed in ‘other rented accommodation’ in 2019. This meant that demand driven by this subcategory had been increasing year-on-year until the tourism sector was hit hard by COVID-19 in 2020. Consequently, total additional user demand turned negative in 2020 as the decrease in demand by short-stay visitors outweighed the additional demand by first-time buyers and foreigners (see graph).

Turning to housing supply, it is defined as the quantity of housing in existence. These come onto the market following a process initiated through the application for a building permit with the Planning Authority (PA), followed by its approval. Approved permits translate into additional housing stock on the market with a certain lag as it takes time to construct new housing units. In 2018 and 2019, around 20,000 permits were approved, meaning that such housing units would then come onto the market in one/two years’ time.

Source: ‘The Malta Property Landscape: A True Picture’, Grant Thornton and Dhalia, June 2022

Between 2013 and 2019, additional demand significantly exceeded additional supply. However, during 2020 and 2021, additional housing supply by far outstripped additional demand, putting downward pressure on house prices. In fact, during this period, house price growth grew at a much smaller pace than it did pre-COVID (see Selling house prices in Malta).

Based on the number of permits issued by the PA, Malta’s demography and forecast economic growth, the outlook for the three years ahead foresees a slowdown in additional housing supply and recovering housing demand. These developments are expected to ease, but not eliminate the downward pressure on prices as additional demand will likely not suffice to fully meet the supply of housing that would have been accumulated by 2024.

Having said that, recent international developments, such as the Russian invasion of Ukraine, compounded with the lingering effects of COVID-19, complicate the outlook for the housing market. European Union Member States report that construction costs have increased by 20% - 30% due to the negative impact that such factors have had on the global economy. This is also evident locally as reports suggest that the average cost of raw materials have increased by 30% - 40%. These developments are expected to push prices upwards in the immediate term and will impact housing demand and supply in the medium to long-run.

Furthermore, housing demand and supply are likely to be impacted by the Eurozone interest rate rise in response to high rates of inflation. This implies higher borrowing rates for both first-time buyers and investors. The effect of this factor is expected to be reflected in the medium run, as house prices are typically ‘sticky’ to changes in the interest rate.

Taking all these factors into account, the future of the housing market looks challenging.

The Malta Property Landscape: a true picture

The 'Malta property landscape: a true picture' is a biannual publication bringing together Dhalia’s high-quality data on the real estate market and the analytical expertise of Grant Thornton Malta. The report provides in-depth analysis and timely information on developments in the Maltese property market to allow policymakers, businesses and people investing in property to make informed choices.

For more information on the report please visit The Malta Property Landscape | Grant Thornton Malta

George Vella