How blockchain could change the financial and legal industries and the world at large.

If someone in 1993 would have said that the Web would be integral to our life today, would you have believed them? After steam, electricity and computing, it is the common creed that blockchain will soon become a symbol of the next industrial revolution. Industry experts proclaim the emerging technology as the next big disruptor, with both geeks and fintechs deep in thought and testing. The question is whether it will be a secret behind the scene transformation for the beneficiary industries, or a loud uprising that will make blockchain the next decade’s buzzword.

Few can however argue that blockchain has had little impact on the financial and legal industries. To the contrary, the degree to which the fintech industry has changed over the last decade due to this disruptive technology is off the scale. The world has witnessed the arrival of new currencies, technologies, business models and forms of transactions; all within an environment of global economic upheavals and increasingly comprehensive regulation. Much more is to follow.

Digitalisation has come in overwhelming waves, driven by the growth of e-commerce – first in the B2C, and now the B2B space – and the proliferation of smart devices and internet of things (IoT). With it has come continuous innovation to meet the demand for technologies that drive efficiency, lower transaction costs and boost convenience. Innovative and nimble new players, particularly fintechs and digital ecosystems, have entered the payments and transactions game, creating increased competition for traditional banks and financial institutions.

The European Union is also taking a keen interest in Blockchain. Testament to this is the July 2016 EC report “Opportunity Now: Europe’s Mission to Innovate,” by Robert Madelin, Senior Adviser for Innovation to EU President Jean-Claude Juncker. The 346-page document highlights blockchain as a fundamental sphere to turn Europe into an innovation leader by creating an environment that spurs the development of stable, safe and reliable blockchain applications in product and service markets through regulatory and commercial competition.

Madelin believes that this will “lead to innovative business models that will broaden the spectrum of innovation beyond pure technological innovation, as they foster process, service and organisational innovation as well.”

What is blockchain technology?

For several decades we have thought of the Internet as a straight exchange of information. Varying assets – ranging from intellectual property to music, from money to publishing, from property deeds to health records – are all controlled by large intermediaries that handle the major processes involved in any one of many transactions. Practical examples include banks transferring money between individuals, businesses and countries, and social media companies holding onto giant depositories of data, video and music streaming services.

There are many transactions involved, both individually and institutionally, that include everything from authenticating, clearing, processing and bookkeeping. But these intermediaries are far from perfect and one of their biggest flaws is centralisation.

They are also slow and take a reasonably large cut from any of the businesses in these value exchanges. The idea behind blockchain is to do away with such centralised transaction systems and offer an alternative that is accessible, easily applicable and more secure.

Blockchain technology’s potential lies in its ability to create a distributed ledger of transactions, of which all participants have an identical copy that can be accessed and viewed in real-time. It can be technically defined as “a distributed, decentralised database technology that maintains a growing list of transactions and, through encryption and other activity, verifies their permanence.” It means that every participant in the process can manipulate the ledger securely and without the need for a central authority, because they all see it simultaneously.

To really get blockchain explained, one can break the system down into its three most important parts: a network of computers/participants, a network protocol and a consensus mechanism.

Depending on the permissions of the blockchain, it can be public, and open to anyone with a computer, or private, accessible only by specific members. Each computer is called a node, and it makes up one part of the network of participants in the blockchain.

A network protocol is, in plain English, a rule book that determines how those nodes can talk to each other. Typically, each node has its own copy of the general ledger (the blockchain) so there’s protection against mistakes or fraud. That redundancy, called “fault tolerance,” is what makes blockchain unique.

The consensus mechanism is the process by which a blockchain network verifies transactions and comes to an agreement on what the current, accurate blockchain is. Such rules are agreed upon beforehand by every node in the network—they’re a defining feature of the network. Anyone, individually, can check the validity of each transaction and come to a conclusion on whether it’s good or not. Since anybody can securely check any proposed transaction against this shared ledger, this approach permits participants to have confidence in the integrity of any single entity.

Public blockchain networks tend to have pretty high standards for security, while private networks might be a little more trusting. But either way, the rules that form the consensus mechanism are what gives blockchain technology its flexibility and power.

Understanding how the system works is complex, but one should be more interested in its application and benefits.

Bitcoin and digital currencies

One of the first implementations of blockchain was Bitcoin followed by a number of other cryptocurrencies – but none as widespread to date. Bitcoin made its debut in relative obscurity at the start of 2009, when the financial crisis was still raging. The bitcoin protocol and reference software was created by a person or group of persons known as Satoshi Nakamoto and released as open-source software. The idea was to take power out of the hands of the central bankers and governments who usually control the flow of currency.

Bitcoin and similar digital currencies operate through the setting of distributed ledgers that allow individuals to exchange electronic money securely without necessarily having the transactions settled centrally through a bank. Such level of decentralisation ensures that no single institution controls the bitcoin network. Cryptocurrencies also ensure great transparency, since the history and details of every single transaction that ever happened in the network is stored and can be traced back to the point where the digital currency was produced.

What’s not great about cryptocurrencies? Over the past years, we have seen that these exchanges can be vulnerable to hacking, though the latest methods have seen a very strong improvement in terms of security. The fact that cryptocurrency allows a fair level of anonymity for the account holders isn’t a selling point for authorities either.

Some argue that being relatively unregulated, cryptocurrencies, with bitcoin in particular, could potentially be at the heart of illegal activities, including tax evasion or money laundering. The new EU Anti-Money Laundering Directives (AMLD) which are currently being finalised are meant to conciliate such concerns and clamp down on illegalities.

This will also be enforced by the EU’s action plan to strengthen the fight against terrorist financing, through which the Commission is proposing to bring anonymous currency exchanges under the control of competent authorities by extending the scope of the AMLD to include virtual currency exchange platforms and have them supervised under Anti-Money Laundering/countering terrorist financing legislation at a national level.

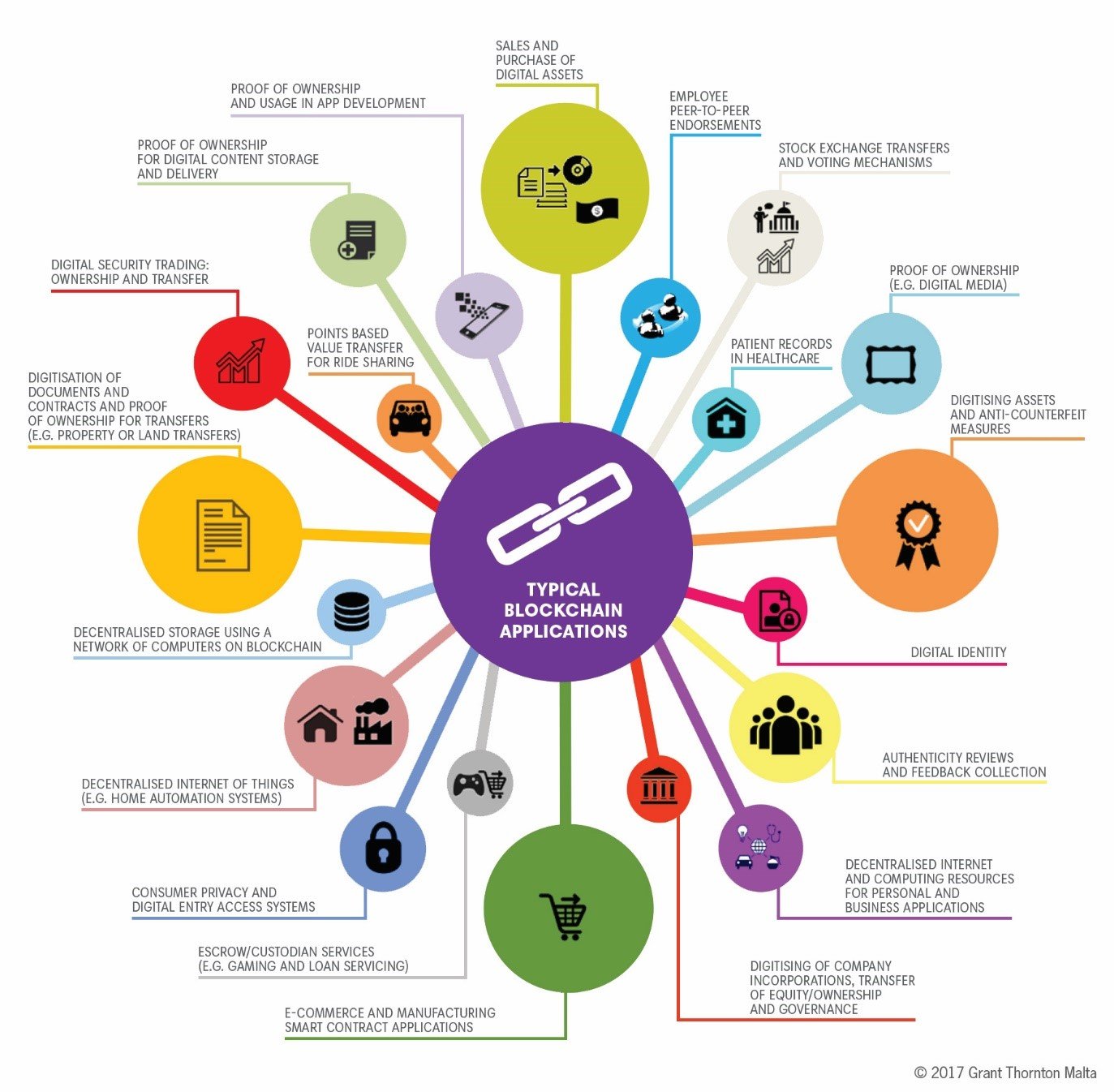

Blockchain applications

A broad range of innovators are creating solutions beyond cryptocurrencies using blockchain technology.

Digital content like music, movies, and online ads could use blockchain to prevent piracy. By using new file formats that can play the media and encode blockchain data that reflects intellectual property and payment history, musicians and filmmakers wouldn’t be losing out on millions.

Looking at healthcare, Blockchain technology has the potential to transform health care, placing the patient at the centre of the health care ecosystem and increasing the security, privacy, and interoperability of health data. In medicine, blockchain technology is being used in the US and Estonia to prevent the theft of pills through the supply chain and give medical history ownership back to patients - who can distribute it to their doctors, for certain amounts of time, as they want or need. In the health sector, blockchain is being considered as a solution to the counterfeiting of drugs.

In the food and drink industry, farmers could use blockchain to monitor their crops—and trace where and when food recalls occur.

![Typical Blockchain applications schema]()

Disrupting the legal and financial world

Blockchain will also alter the legal landscape primarily through its use for smart contracts - self-executing contractual states, stored on the blockchain, which nobody controls and which are immutable - and therefore everyone can trust. Smart contracts can be pre-programmed with the ability to self-execute and self-enforce themselves.

Identifiable legal industries that are seeing an active use of blockchain technology and smart contracts include IP, land registry and deed management. Some Latin American countries, for example, have already begun to use blockchain as a means to keep track of who owns which land deeds.

Several law firms have also started to make a foray into the blockchain space. Recently Steptoe & Johnson, a US legal firm, began a multi-disciplinarian practice to help manage the blockchain for clients. They will also be accepting Bitcoin as payment. Most importantly, they co-founded the Blockchain Alliance, a coalition of 25 blockchain companies and 25 regulatory and law enforcement agencies — including Interpol, Europol, the Securities and Exchange Commission (SEC) and the FBI — to educate enforcement agencies about digital currencies and blockchain technology.

In some African countries they are looking at using blockchain technology to keep census information. Voter records could also be added to this process as a means to have a central repository of eligible citizens. In this area, which is currently under development, blockchain seems primed for tremendous growth.

What about blockchain applications within the financial world?

Whilst digital currency applications are the best known to date, banks and financial services are using blockchain to cut out the middlemen, save time and money, whilst reducing risk when dealing with monetary transactions.

The potential of blockchain is so powerful that nine major banks, including JP Morgan and Goldman Sachs, have joined partnership with one another to invest and develop the technology. Santander estimates that blockchain can save banks up to $20 billion a year in infrastructure costs by eliminating central authorities and bypassing slow, expensive payment networks.

The insurance industry could also dramatically change. The sector is employing blockchain technology when registering luxury assets to help prevent theft and fraud. One project - which involves Interpol, insurers and diamond distributors - is working to stem the flow of ‘blood diamonds’ into the precious-stones market. Another project is looking into the use of blockchain to provide the opportunity for individuals to get insurance that lasts for a few hours, such as sports insurance.

Completely unrelated, Uber drivers are looking into bypassing insurance companies by combining their money together on a blockchain and creating a safety net for themselves. Fraudulent claims, manual processes, fragmented data sources, policies for one user sitting in silo and legacy underwriting models are some of the biggest challenges experienced in the insurance sector today – all causing low customer satisfaction.

Creating policies as smart contracts on the blockchain is an ideal use case for insurance. It offers complete control, transparency and traceability for each claim and could lead to automatic pay-outs. Blockchain technology would also improve risk modelling for the sector, break down the existing silos and significantly reduce fraudulent claims by capturing the origin and ownership of diamonds, paintings, homes, cars and other assets to be insured.

Blockchain and asset management

Asset management will also be a key beneficiary of the blockchain. Traditional trade processes within asset management can be slow, manual, cumbersome and filled with risk when reconciling and matching – and they’re getting more complex with cross-border transactions and for non-standard investment products, such as loans. Each party in the trade lifecycle (e.g. broker-dealers, intermediaries, custodians, clearing and settlement teams) currently keeps their own copy of the same record of a transaction, creating significant inefficiencies and room for error.

Blockchain technology simplifies and streamlines this entire process, providing an automated trade lifecycle where all parties in the transaction would have access to the exact same data about a trade. This would lead to substantial infrastructural cost savings, effective data management and transparency, faster processing cycles, minimal reconciliation and the potential removal of brokers and intermediaries altogether.

Blockchain technology also has infinite potential when it comes to clearing and settlement in the capital market space, with applications by stock exchanges where blockchain technology allows them to reconcile, settle and pay out dividends based on the stock ownership by people and by organisations that are already in place.

The accountancy world will not go untouched. Accountants do a lot of transaction processing, reconciliation and control, and that could change significantly if this technology gets adopted on a widespread basis. The cost savings that financial institutions are looking at are huge, and most of that saving will come from people who do the back office. Be it accountants or ledgers, there’s a degree of challenge to those in the accounting profession who work in finance functions.

The nature of auditing could also change, by removing some of the more transactional and checking parts of the role. Blockchain could provide a third validation point which does not exist so far. With blockchain technology validation could be provided independently, potentially by an independent network validating transactions that have been recorded on the blockchain. The role of audit could move further up in the value chain, into providing more of a governance role around the various types of blockchains that are going to be used.

![Smart contracts schemas with blockchain technology]()