Housing affordability in Malta

29 Jul 2022By Rachel Bonett, Economic advisor at Grant Thornton

In recent years, concerns about housing affordability in Malta have become more pronounced due to the escalation in property prices.

In essence, housing affordability relates to an individual’s ability to pay for housing – a basic human need. When housing affordability is being discussed, one could consider whether an individual is able to rent a property; or their ability to purchase a property in their lifetime. Here we are talking about the latter.

Since most first-time buyers rely on bank borrowing to finance the purchase of their house, one way to measure affordability is to measure the buyers’ borrowing capacity. The maximum house price that a household can afford will depend on the household’s income; the prevailing borrowing rate; and other leverage requirements. Other leverage requirements could include required down payments, for instance, in Malta, a 10% minimum down payment is generally required by commercial banks for first-time buyers.

If the market price of an average property exceeds the maximum affordable house price level, then the average household would have affordability problems.

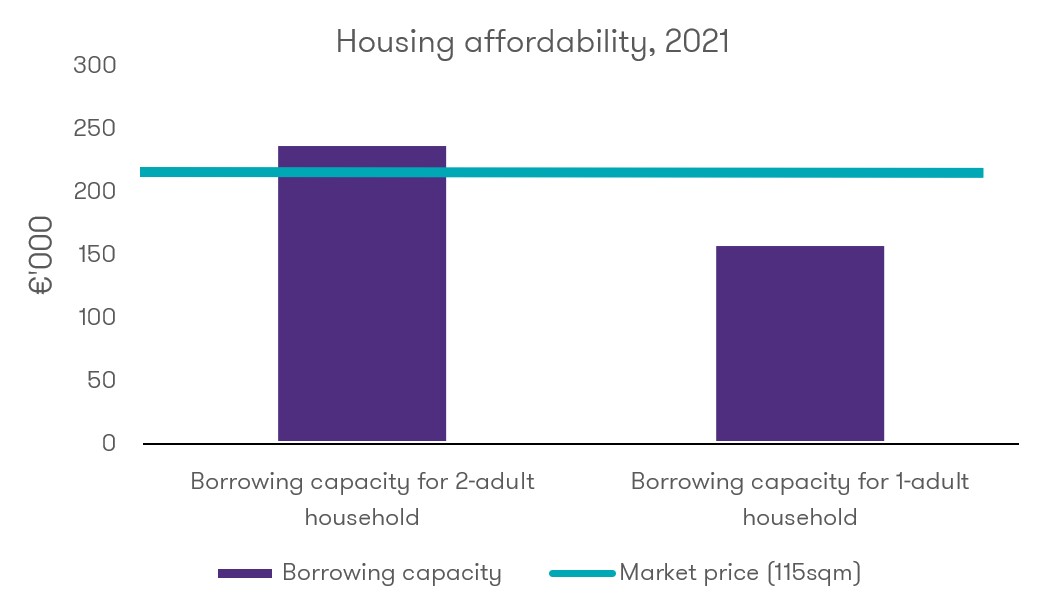

The number of individuals in a household who receive an income will have a big effect on their affordability. Consider two scenarios, a two-adult household where the joint net annual salary is €38,155, and a one-adult household with a net annual salary of €25,436.

As presented in the chart, in the year 2021, the average market price for a 115 square metre finished apartment was €215,000, as indicated by the horizontal line. Taking borrowing capacity into consideration, assuming the 10% minimum down payment has been saved, the two-adult household and one-adult household would be able to afford a property worth a maximum of €240,000 and €160,000, respectively.

This means that, the two-young adult household could just about afford the average 115 square metre apartment. However, the same cannot be said for the one-young adult household, as the maximum affordable house price falls significantly short of the prevailing market prices. This means that the individual would not be able to afford the property based on their ability to borrow money from the bank.

Source: ‘The Malta Property Landscape: A True Picture’, Grant Thornton and Dhalia, June 2022

Having said this, one should exercise caution when interpreting such results. Firstly, a significant number of two-young adult households have incomes which fall below the median income, thus making the average sized unit unaffordable to them. Moreover, this calculation is based on finished and not furnished apartments. When assessing housing affordability, one should also consider the added expenditure inevitably incurred by the household to furnish their apartment which does not feature in this calculation.

In conclusion, affordability issues in Malta persist and pose a significant burden on future homeowners. This may potentially drive first-time buyers out of the housing market.

The Malta Property Landscape: a true picture

The 'Malta property landscape: a true picture' is a biannual publication bringing together Dhalia’s high-quality data on the real estate market and the analytical expertise of Grant Thornton Malta. The report provides in-depth analysis and timely information on developments in the Maltese property market to allow policymakers, businesses and people investing in property to make informed choices.

For more information on the report please visit The Malta Property Landscape | Grant Thornton Malta

George Vella