GAPSME: general accounting principles for individual and group companies

15 May 2020Applicable Accounting Framework

The EU Single Accounting Directive 2013/34/EU which substituted the Fourth and Seventh Directives on both individual and consolidated financial statements, introduced a new set of financial reporting requirements. This Directive was transposed into Maltese law through the introduction of the General Accounting Principles for Small and Medium-Sized Entities (GAPSME).

GAPSME has become the default accounting framework for SMEs for financial reporting periods starting on or after 1 January 2016. Nonetheless, the directors of small or medium-sized entities may still elect to apply International Financial Reporting Standards (IFRS) as adopted by the EU, if the Board of Directors or its governing body, has passed a resolution to this effect.

Objective of GAPSME

The objective of GAPSME is to ensure that the reporting entities or groups falling within its scope provide in their financial statements information about the financial position and performance of the entity or group that would be useful to users in assessing the stewardship of management and for making economic decisions.

Individual Accounts

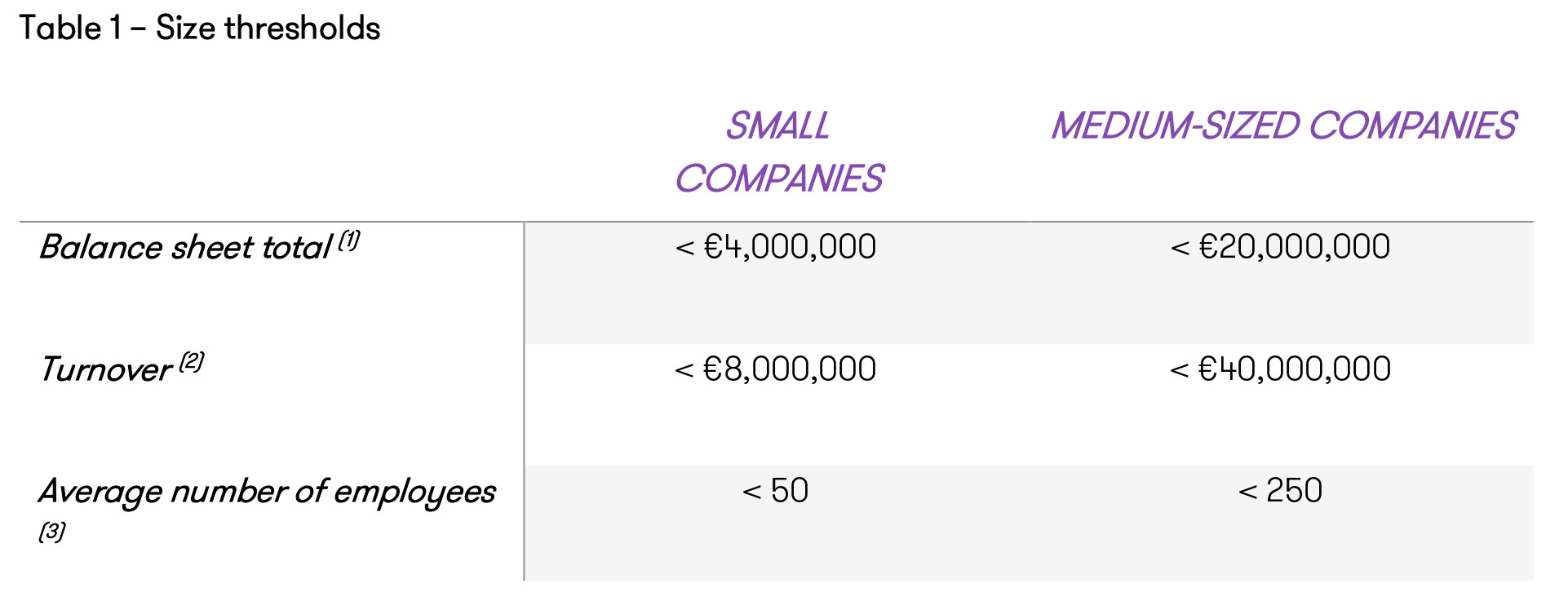

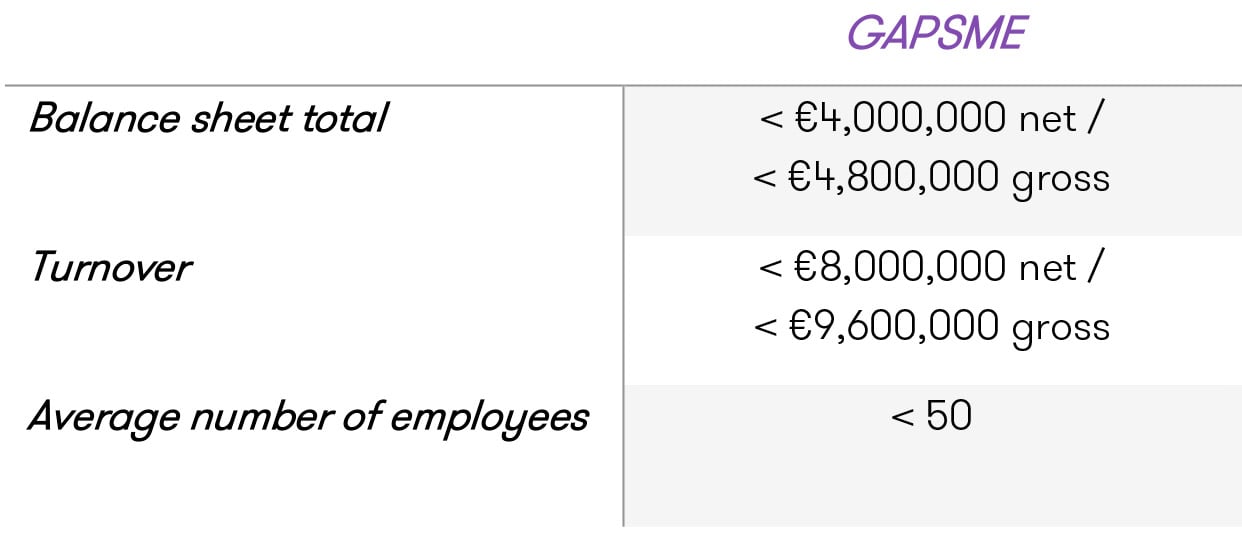

Size Thresholds

On the balance sheet date, in order for an entity to be classified as small and medium, two out of three of the below criteria in Table 1 must be satisfied, with the exception of Large and Public Interest Entities (PIEs) as PIEs are treated as large regardless of their size.

(1). The balance sheet total represents the total value of assets held by an entity, including those that are current and non-current.

(2). In the EU Accounting Directive, turnover is defined as the amounts derived from the sale of products and the provision of services after deducting sales rebates and value added tax and other taxes directly linked to revenue.

(3). In determining the number of average employees:

i. In relation to whole-time employees, the aggregate number of full weeks worked by all the whole-time employees of the entity during the financial reporting period, divided by the number of full weeks comprised in that financial reporting period, rounded off to the nearest number; and

ii. In relation to part-time employees, the aggregate number of hours worked by all the part-time employees of the entity during the financial reporting period, divided by the number of full weeks comprised in that financial reporting period and again divided by forty, rounded off to the nearest number.

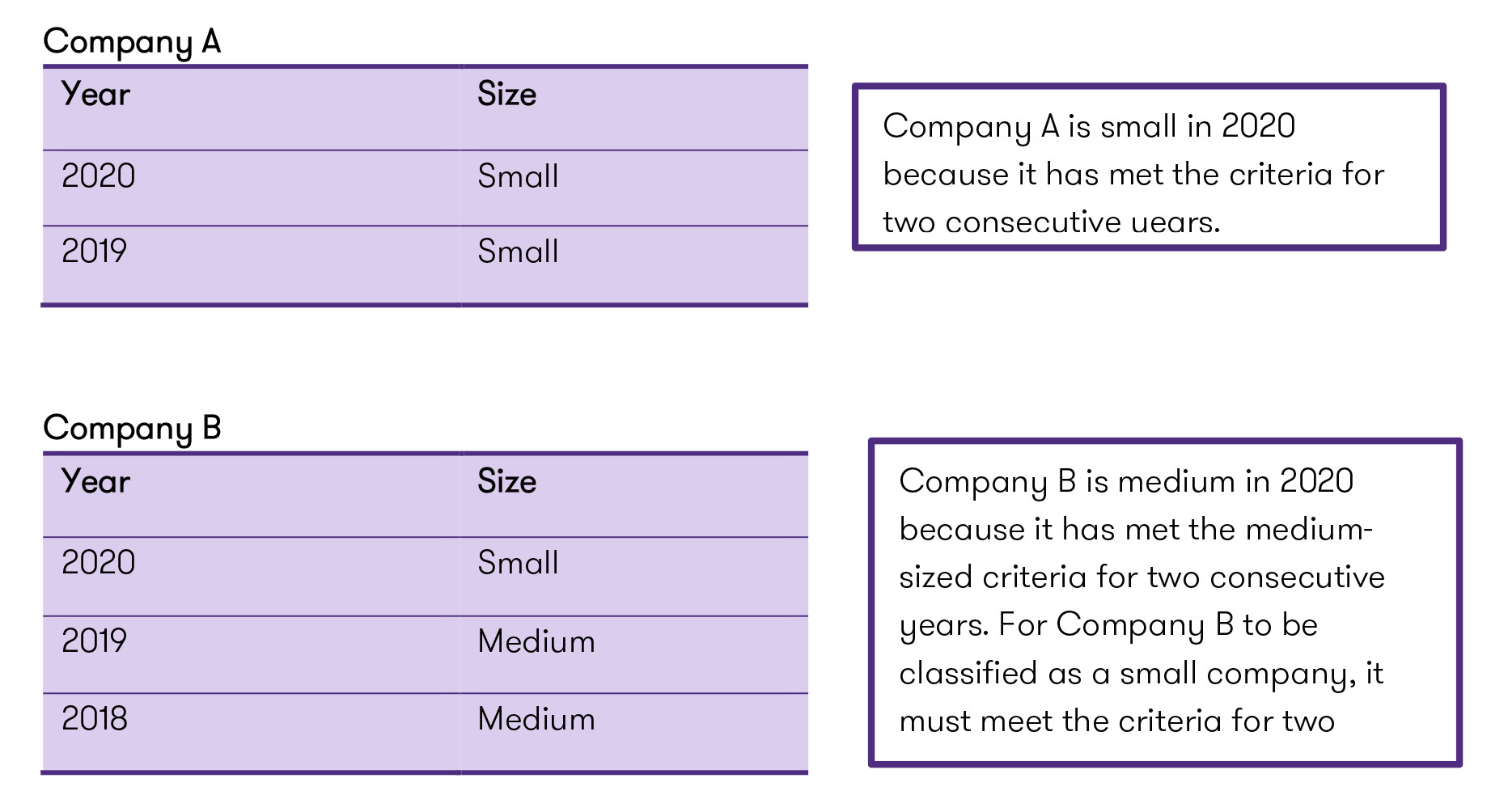

The thresholds affect the designation of a company as small, medium, or large by reference to two consecutive accounting periods. A newly incorporated company will determine whether it qualifies as small, medium-sized, or large by reference to Table 1 in that year.

The following examples illustrate the application of the above:

Presentation of financial statements

A complete set of financial statements must comprise of the following:

- a balance sheet;

- an income statement; and

- notes to the financial statements.

A statement of changes in equity and a statement of cash flows must also be prepared for medium-sized entities.

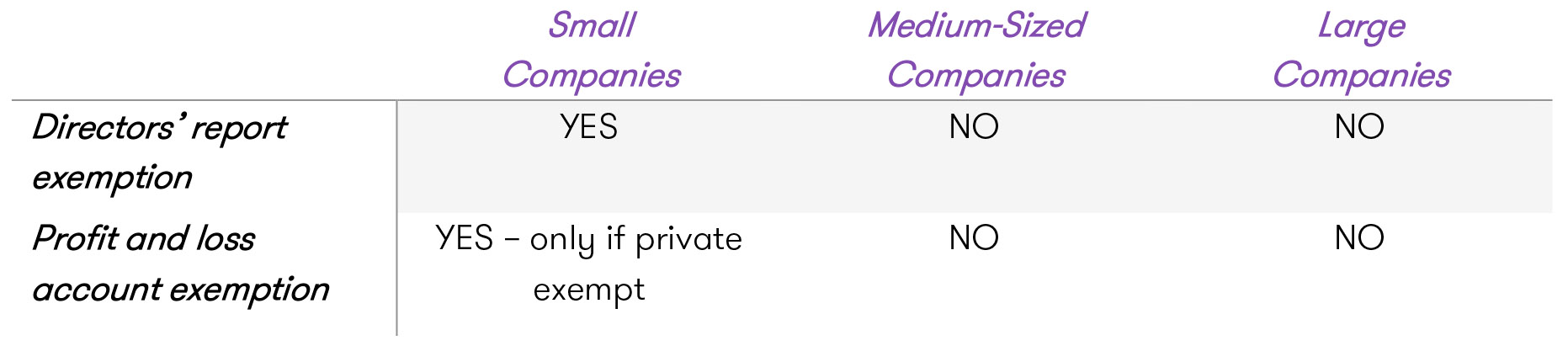

Exemptions

Small companies other than PIEs are exempted from delivering a directors’ report to the Registrar. When the directors take advantage of this exemption, they are required to sign and deliver to the Registrar a declaration confirming that the company qualifies for the exemption.

A small company that is private exempt is eligible for the exemption from submitting a profit or loss account with the Registrar. If the exemption is applied, a declaration must be signed and delivered to the Registrar by the same directors who signed the balance sheet, together with the annual accounts which will confirm that the company qualifies for the exemption.

Consolidated Accounts

Consolidated financial statements are the financial statements of a group presented as those of a single economic entity. An entity which controls one or more entities is required to prepare consolidated financial statements.

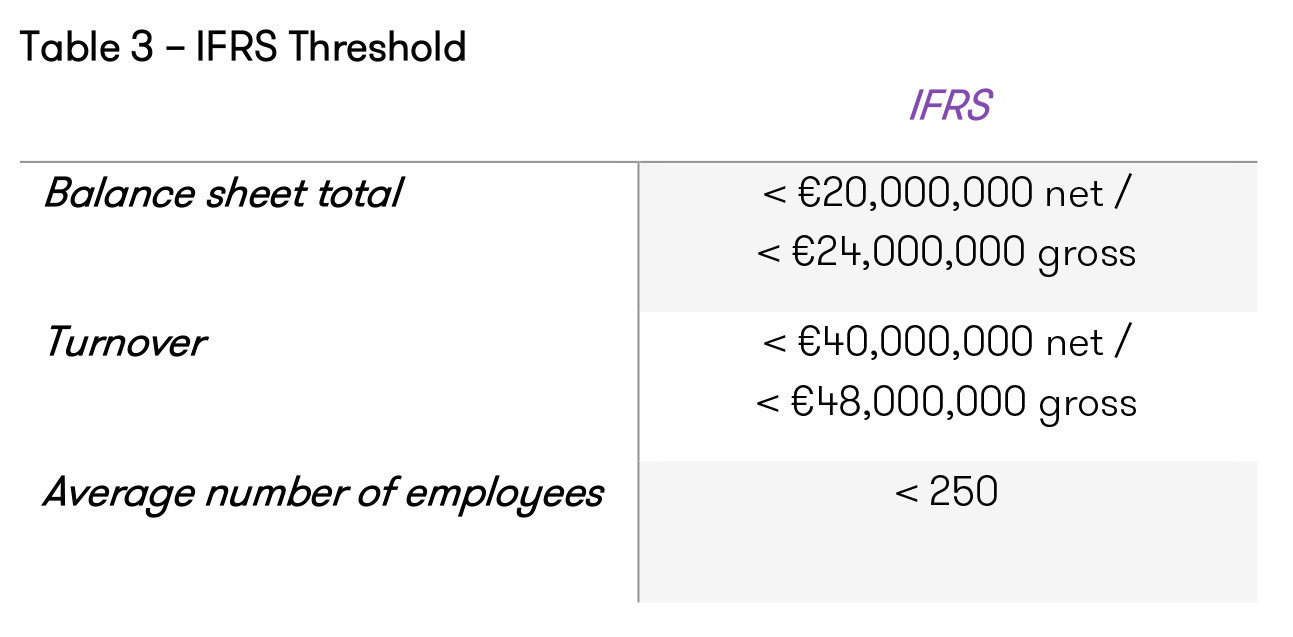

GAPSME or IFRS?

In terms of Maltese law, by default all parent companies are required to prepare consolidated accounts under IFRS or GAPSME. The group must use IFRS to prepare the consolidated financial statements if the group figures exceed any two of the three of the below criteria in Table 3 as at balance sheet date. If any two of the below criteria are not exceeded, the group can prepare consolidated financial statements under GAPSME.

Exemption from consolidation

Unlike IFRS, GAPSME provides for an exemption from consolidation where the parent and its subsidiaries do not exceed at least two out of three of the below figures as shown in Table 4.

Table 4 – Consolidation exemption

The above criteria must be satisfied for two consecutive years for the group to be exempt from preparing the consolidated financial statements.

Notes:

Gross – Gross shall mean that the group turnover and total assets shall be computed without any setoffs and other adjustments required for consolidation.

Net – Net shall mean that group turnover and total assets shall be computed after consolidation adjustments have been affected.

Consolidated financial statements

If, in certain circumstances, one or more of the subsidiaries to be consolidated are prohibited from applying GAPSME in the preparation of their individual financial statements, the group may nonetheless prepare the consolidated financial statements in accordance with GAPSME provided that the below information is disclosed in the consolidated financial statements:

- the fact that a subsidiary has prepared financial statements in accordance with a financial reporting framework;

- the name of the relevant subsidiary; and

- the financial reporting framework under which those financial statements have been prepared.