VAT in the Skies: When the Exemption Does Not Apply

Navigating VAT in the Skies:

Aircraft Leasing and Leasing Chains

QUICK SUMMARY

In Part 1 of this series, we explored how international passenger transport enjoys a specific VAT exemption under Maltese law and the EU VAT Directive. But airlines do more than transport passengers, they need aircrafts to operate. In today's aviation industry, ownership is rarely straightforward. Instead, airlines rely heavily on leasing arrangements, and this is where VAT treatment becomes far more complex.

Dry Lease vs Wet Lease

In the aviation sector, the two most common types of leases are dry leases and wet leases, each carrying different VAT considerations:

- Dry Lease - The lessor provides only the aircraft, leaving all operational responsibilities (crew, maintenance, insurance) to the lessee. This is essentially a "bare aircraft hire".

- Wet Lease - Also known as ACMI (Aircraft, Crew, Maintenance, and Insurance), this arrangement goes further. The lessor provides both the aircraft and the crew, while also retaining responsibility for maintenance and insurance.

From a VAT perspective, distinguishing between the two is crucial. A wet lease more closely resembles a transport service, while a dry lease is seen as a supply of goods or the long-term hiring of a means of transport.

VAT Exemption on Aircraft Supply

Maltese VAT law, specifically, Item 7(1) of Part One of the Fifth Schedule and Article 148(f) of the EU VAT Directive provide a VAT exemption for the supply of aircraft, but only if certain conditions are satisfied:

- Airline Status: The recipient must be an airline holding an Air Operator's Certificate.

- For Reward: The airline must operate on a commercial basis, not for private or recreational use.

- Chiefly for International Transport: A substantial portion of the airline's operations (generally interpreted in practice as over 50-60%) must involve international travel.

If all three conditions are met, the supply of the aircraft may be VAT exempt, whether structured as a dry lease or a wet lease. If not, the transaction falls within the standard VAT rate.

VAT in Leasing Chains

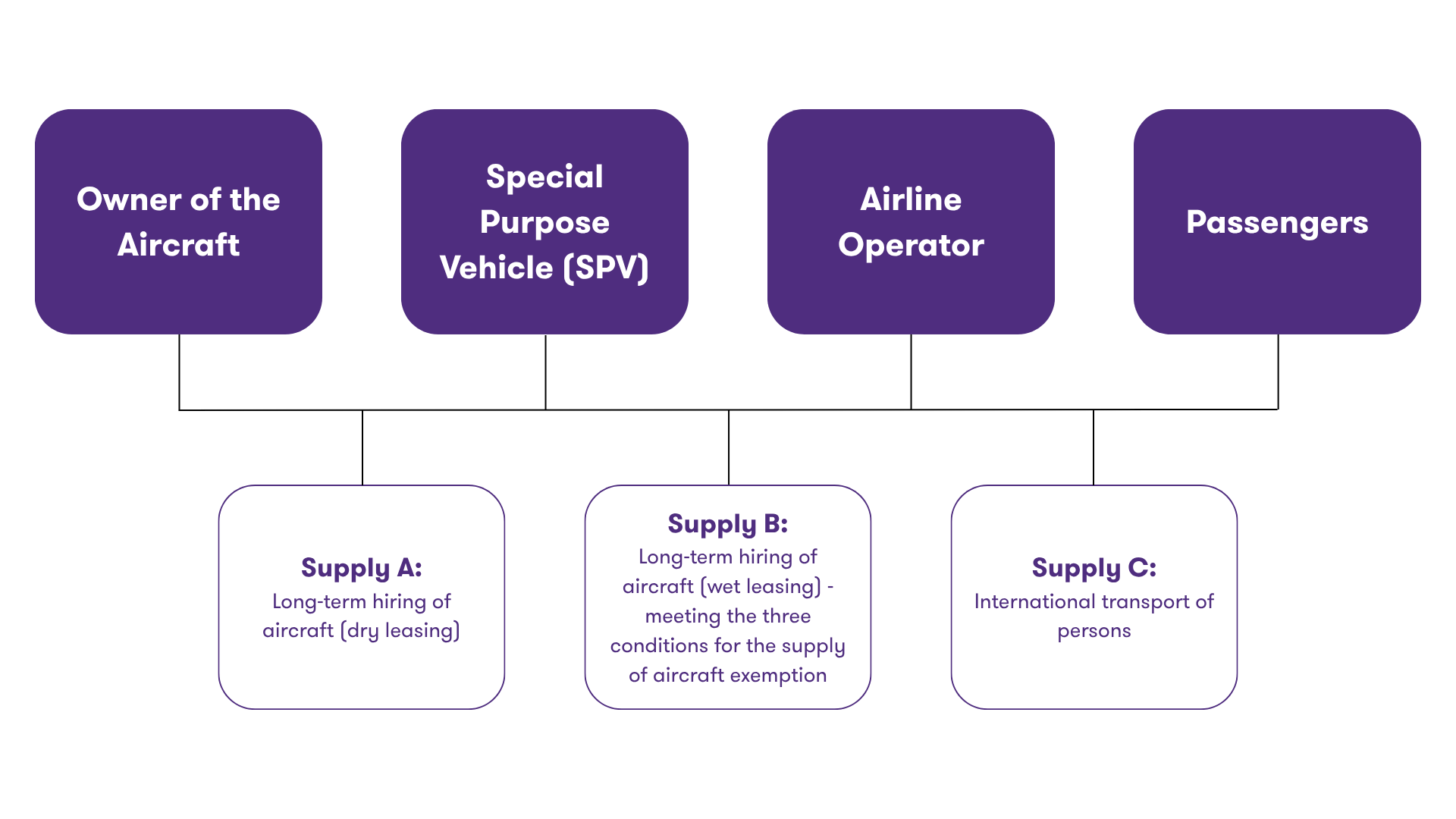

In reality, aircraft are often leased through multiple entities before reaching the airline. A common type of transaction involves the below chain of entities:

Supply A:

This is typically a dry lease provided by the aircraft owner to an SPV. The SPV itself is not an airline operator and does not use the aircraft for reward or for international transport. As such, the supply may not meet the conditions for exemption under Item 7(1) of Part One to the Fifth Schedule of the VAT Act and are therefore generally subject to the standard rate of VAT. If the lease is short-term, which is less than 30 days for VAT purposes, the place of supply would be where the aircraft was made available to the customer. Conversely, if the lease is for more than 30 days, the place of supply would be where the taxable customer is based (general B2B rules for place of supply).

Supply B:

In this second transaction, the SPV sub-leases the aircraft to an airline operator that holds a valid Air Operator's Certificate (AOC) and uses the aircraft for reward and chiefly for international transport. Provided all three conditions are met, this supply may be treated as exempt with credit. The exemption is applicable irrespective of whether the lease is dry or wet, as long as the recipient qualifies and the use of the aircraft satisfies the aforementioned conditions. In the case that such conditions are not met, the supply would be subject to the standard rate of VAT.

Supply C:

The airline then uses the aircraft to transport passengers, for instance from Malta to Italy. This service falls within the exemption for international transport of passengers, and thus no VAT should be charged to the customers, regardless of their status as taxable persons or non-taxable persons.

Key Insight

Each step in the leasing chain must be assessed on its own. Exemptions cannot simply be "looked through" to the final use of the aircraft - a supply to a non-airline entity may still attract VAT, even if the aircraft ultimately ends up flying international passengers.

Conclusion

The VAT treatment of aircraft leasing depends not only on the type of lease but also on the status of each party in the leasing chain. This layered approach is what makes VAT in aviation uniquely complex and why careful analysis is essential in every transaction.

At Grant Thornton Malta, our VAT specialists understand the intricacies of aviation leasing structure and the regulatory landscape. Whether you are navigating leasing chains, assessing exemption eligibility, or structuring cross-border transactions, our team is here to help you make informed, compliant decisions.

Authors

-

Deon Caruana Deon is a dedicated intern, with three years of experience at Grant Thornton. Starting in the Audit and later in the Tax department, he showcased his exceptional skills and commitment to learning. Now, Deon thrives in the VAT department, where his passion for accounts truly shines.

Deon Caruana Deon is a dedicated intern, with three years of experience at Grant Thornton. Starting in the Audit and later in the Tax department, he showcased his exceptional skills and commitment to learning. Now, Deon thrives in the VAT department, where his passion for accounts truly shines.View Profile

Wayne Pisani

Partner | Head of Regulatory and...

Michael Agius

Partner | Head of Tax, Wealth Management...