ICO: fundamentals and the cryptocurrency tax in Malta

26 Nov 2019Note from the author: reference to 'cryptocurrency' shall be construed as a reference to digital assets including DLT assets, security tokens, virtual tokens, cryptocurrencies and other similar digital assets.

Initial coin offering (ICO) campaigns, sometimes referred to as ‘token sales’ or ‘token-generating events’ (TGE), which use the internet and social media to raise funds for a venture through the issue of a cryptographic token in exchange for digital currency (fiat or virtual) may be paralleled to online crowdfunding campaigns or initial public offerings (IPOs).

The issuer looking for funding typically develops a cryptographic token which is either offered in exchange for one of the already well-established virtual cryptocurrencies (such as litecoin, ripple or bitcoin) with a view to ultimately exchange the raised cryptocurrency funds for fiat currencies or barter them for goods and services required for the project being funded.

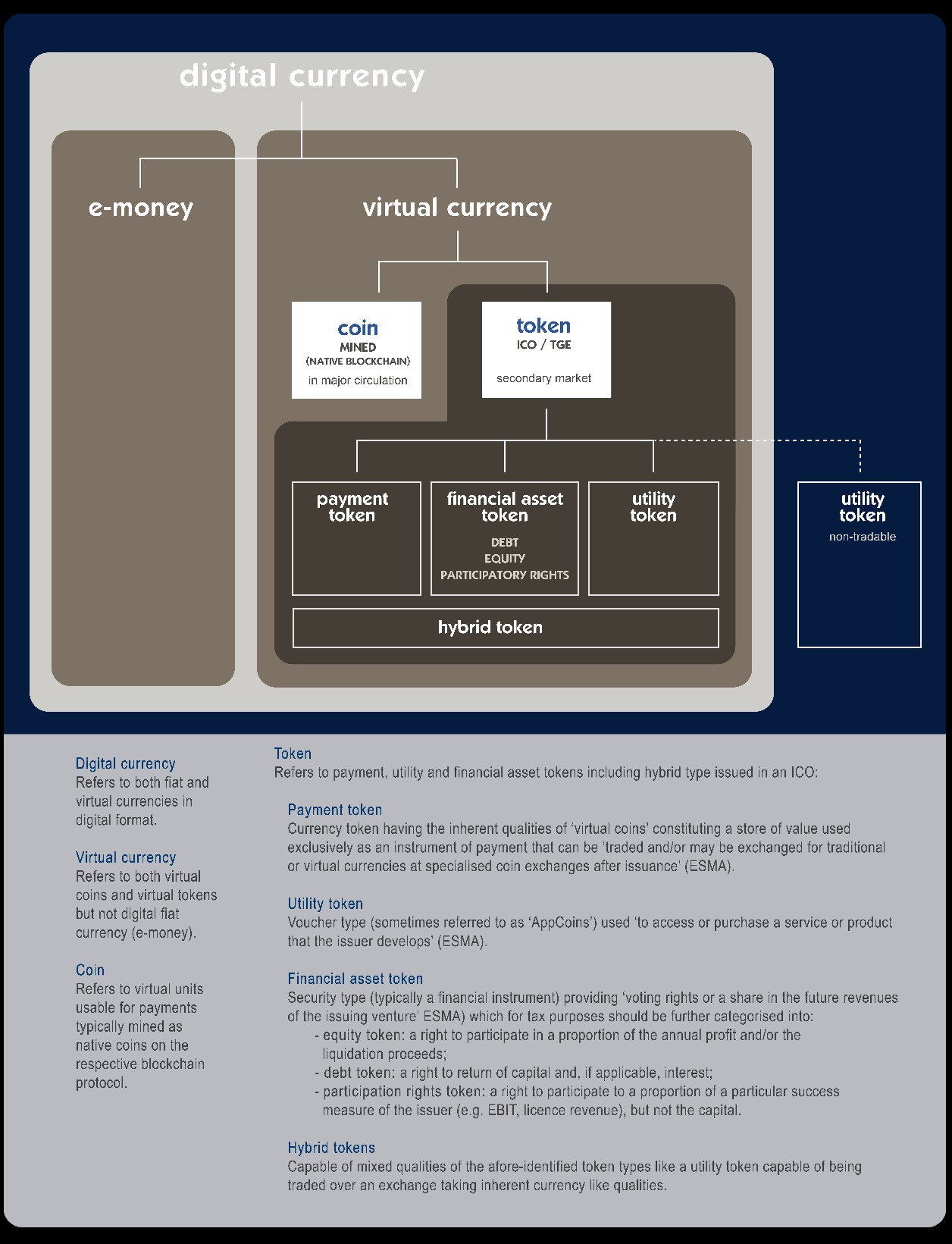

Tokens issued within an ICO context are typically created in the form of cryptocurrency, entailing the ability to be used as a medium of exchange[1], and disseminated using distributed ledger or blockchain technology in the shape of an independent monetary base. The collective term ‘virtual currency’ refers to two principal types of virtual units, namely:

- tokens generated in an ICO representing a particular fungible and tradable asset or utility

- coins mined via the calculation of cryptographic hashes to solve complicated mathematical problems called ‘proof of work’, having no purpose other than being a means of payment.

At this juncture, it is pertinent to point out the peculiar qualities of ‘currency’ as distinct from ‘money’[2]. Before the advent of governments creating monetised currency, there was barter as currency. Derived from the Latin word ‘currens’[3] and Middle English word ‘curraunt’[4] entailing ‘running, moving along’, the word ‘currency’ means ‘in circulation’. Currency hence entails the ability to be kept in circulation, accepted as a medium of exchange. Gold, silver and salt[5] were an accepted ‘money’ medium for their intrinsic ability to hold value and be broken down into units (by weight) as an independent natural medium of exchange. Currency is an indicator of representative value accepted by a counterparty, a promissory note that can be traded or exchanged in return for goods or services, whilst money is a store of value divisible into units of account. Short of money taking the shape of a commodity, the intrinsic value of representative money is directly contingent on its acceptance as such by a counterparty, making it a medium of exchange recognised as currency in legal tender.

Tokens issued in an ICO would be bereft of value, unless asset backed, were it not for counterparties accepting their representative value as a medium of exchange, making it therefore possible to attribute the term ‘currency’ to them. This research draws on the classification and categorisation of tokens by the Financial Action Task Force (FATF)[6], the Blockchain Policy Initiative Report[7], the European Central Bank[8], the European Banking Authority[9] and the Bank of England[10] amongst others to examine this underlying quality of tokens to act as proprietary payment currencies (Chapter 2).

The cryptocurrency tax

This peculiar quality differentiates ICOs from crowdfunding. In this introductory part, the issuance of tokens in exchange for funds raised in an ICO will be weighed against the established principles of crowdfunding; reward based crowd-funding having features similar to the purpose and role of utility tokens, whilst crowd investing and crowdlending being paralleled to financial asset tokens. The typology of the respective tokens triggers different taxable scenarios for such VFA (Virtual Financial Asset) including the introduction of a cryptocurrency tax, particularly when taking into consideration the currency function being attributed to such token instruments. Hence, a detailed appraisal of the payment, utility and financial asset qualities of a token in the light of applicable direct and indirect tax principles will follow, identifying the key characteristic functions thereof.

The categorisation forming the basis of this study is depicted in the following diagram.

Diagram 1 – Digital currencies

ICOs: the sum of the parts

ICOs do not exist in a vacuum. The technology underpinning a transaction should not impact the ancillary transactional tax considerations, and transactions should be governed by the tax principles applicable to equivalent traditional ones. Hence, the regulatory and fiscal arbitrage around the application of the nascent distributed ledger and blockchain technology to financial transactions, particularly ICOs, is gradually subsiding by the issuance of guidance on the application of current legislation.

Tokens can turn everything that we’re used to seeing in paper form – including shares, and money and promissory notes – digital. But the terms we will use for these things will remain unchanged (shares will still be shares). The fact that crypto assets are stored in a decentralized accounting system, or require digital signatures, doesn’t change their meaning or value.[11]

It follows that although the majority of the jurisdictions may not have specific ICO regulations, this does not mean that all ICO offerings are permissible. Existing financial laws such as securities and collective investment scheme regulations, prepaid payment instrument regulations as well as financial instrument exchange regulations may apply to some kinds of ICOs. Failing that, the foundational laws such as civil law, commercial transaction law, consumer protection law, and criminal law should be applied to ICOs.

In its guidance note on cryptocurrencies, the United Kingdom (UK) Her Majesty’s Revenue & Customs (HMRC) stated that the tax treatment of any transaction involving the use of cryptocurrencies is to be ‘looked at on a case-by-case basis taking into account the specific facts’, each case being ‘considered on the basis of its own individual facts and circumstances.’[12]

The peculiar terms of an ICO, including the rights and entitlements attached to the issued tokens, are typically prescribed in a document, referred to as a whitepaper, publishing basic information on the terms of issue, similar to the prospectus in an IPO. The token issued in an ICO would typically represent a balance on an account as stipulated in the whitepaper compiled and presented by the issuer.

This token financialises value directly and allows for liquid secondary markets of exchange. This value can be fractionalised to allow any level of participation down to the smallest of micro-transactions. In principle anyone, anywhere, can participate in these new digital economies before, during, or after they have been created; allowing all parties to have a stake in their success through a form of decentralized ownership.[13]

The Gibraltar Financial Services Commission described ICOs as ‘an unregulated means of raising finance in a venture or project, usually at an early-stage and often one whose products and services have not yet been significantly designed, built or tested, let alone, made operational or generating revenue. Such forms of crowdfunding are often used by start-ups to bypass the rigorous and regulated capital-raising process required by venture capitalists or financial institutions. In an ICO, tokens are sold to early supporters of a project in exchange for cash or cryptocurrency, such as bitcoin or ether.’[14] Such a definition triggers consideration as to whether, at seed funding stage, the issuer can be deemed to be carrying out a trade or business with ancillary tax consequences[15]. The list of qualifiers developed by the UK HMRC[16], generally referred to as badges of trade[17], may be used to make the necessary assessment:

- profit-seeking motive;

- the number of transactions;

- the nature of the asset;

- the existence of similar trading transactions or interests;

- changes to the asset;

- the way the sale was carried out;

- the source of finance;

- the interval of time between purchase and sale;

- method of acquisition.

The subsistence of multiple of the foregoing factors is construed as corroborative of the existence of trading, entailing a trading or economic activity subject to direct and indirect taxation.

Similar to the Gibraltarian descriptive approach, the Swiss Financial Market Supervisory Authority (FINMA), whilst acknowledging that ‘various links to current regulatory law may exist depending on the structure of the services provided’, given that ‘there is no catch-all definition’, attempted an ICO definition by reference to commonly resorted to ICO practices:

Under the usual procedure for ICOs, financial backers will transfer a certain amount of cryptocurrency to a blockchain-generated address supplied by those organising the ICO campaign. In return, financial backers receive blockchain-based coins or other tokens connected with a specific project or company run by the ICO organisers.[18]

FINMA’s approach does not restrict its definition of ICOs by reference to issuers in early-stage funding (start-ups) and defers the regulatory standpoint to be assessed on a case by case basis, depending on the structure of the ‘blockchain-based cryptocurrency or other tokens’ and ancillary investors’ rights.

The peculiarity of the tokens - the constitutive parts

Tokens are, in terms of their content, purpose, rights and duties of their holders, and consequently also incentives of the holders, substantially different. … A token can represent many things and consequently simplification and unification of tokens is wrong, harmful and contrary to the events taking place in the industry.[19]

Although an issued token may not carry any traditional shareholders’ rights, this may nonetheless have speculative characteristics if it is transferable and is listed on a cryptocurrency exchange enabling trading on secondary markets. Such exchange can be for currency (virtual or real), services and products of the issuer of the token (once such products and services are developed) and possibly even profit participation rights.

The analysis of the legal relationship between the issuer and the investor as well as the qualification of the token are fundamental to address possible cryptocurrency tax arbitrage arising from the different treatment of a token transaction by the issuer and the investor. Hence, the underlying regulatory and ancillary fiscal implications of an ICO transaction are directly contingent on the role, purpose, features and peculiar characteristics of the issued tokens, evolving throughout their lifespan from a fundraising function for the development of future products and services to a means of payment for such services.

The inherent ability of a token to be accepted as a medium of exchange is key to the success of an ICO. In principle, all tokens in an ICO can act as an independent monetary base. However, the currency qualities of an instrument of payment are also to be confronted with the peculiarities of secondary market trading, particularly money markets. All tokens traded on an exchange are attributed financial instrument qualities akin to those of an asset or security token enabling trading in the marketplace based on counter acceptance of value by the parties to the transaction. Traded securities, although having the unitised store of value qualities of money (i.e. a number of shares having a quantifiable value), lack the intrinsic qualities of currency as a widely accepted medium of exchange discussed beforehand. In fact, listed securities are typically traded for fiat currency, but not with one another. Hence, notwithstanding the claim that tokens admitted to trading on multiple exchanges may also be ascribed currency like features, this is still to be distinguished from pure currency-type payment or value tokens that have no other utility than to be used as a means of payment[20].

All the foregoing incarnations of tokens trigger different cryptocurrency tax consequences; a payment token might be VAT exempt[21] but a utility token entitling the holder to goods or services which can also be used as a proprietary monetary base (thus a token having payment-type attributes) is likely to have VAT consequences. Furthermore, situations where the investors acquiring the tokens are entitled to a share of profits or a fixed return, akin to a securities issue, are to be weighed against an ICO issuer of payment tokens, akin to trading in coins. The tax arbitrage resulting from the tokenisation of different roles, purposes and features of a token necessitates the breaking down of the transactions behind a token into its constitutive elements.

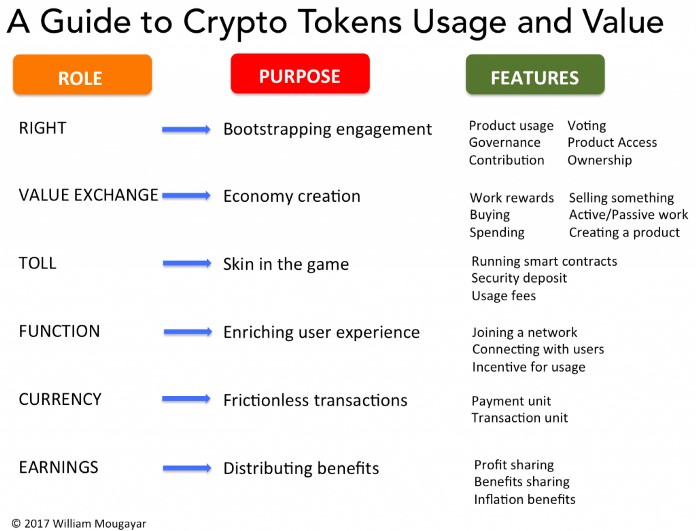

Diagram 2: Token elements[22]

However, notwithstanding the foregoing multifaceted nature of tokens, in the interests of taxpayer certainty, a degree of alignment or harmonisation is also necessary. The classification of ICO tokens into payment, utility, financial asset and hybrid-type as depicted in Diagram 1 is intended to set a degree of clarity for the purpose of this study as well as in the tax assessment of the underlying token transactions. Based on the European Securities and Markets Authority’s (ESMA) definition[23] in its warning statement to investors, a token can take the shape of:

- a unit having a limited intrinsic use providing the key to complete a transaction on a specific blockchain (e.g. a voucher);

- a unit representing assets in the real-world economy (e.g. equity-type);

- a unit representing rights in the real-world economy (e.g. profit-sharing entitlement); or

- currency as a medium of payment.

Some ICO tokens may be likened to a voucher, granting the right to a future service or product being provided by the issuer (utility tokens), whilst others may take the shape of a security-type token - representing equity in a company, a debenture, or a periodical revenue-sharing reward based on the success of a company - more akin to traditional initial public offerings. The challenge with an ICO lies in the fact that different cryptocurrency tax consequences may arise depending on the specific token design and the specific transaction instance in its lifespan, also taking into consideration the private or business status of the investor.

[1] ‘Medium of exchange, something that people can use to buy and sell from one another’, cited from Irena Asmundson and Ceyda Oner, ‘Back to Basics: What Is Money?’ (2012) Vol 49 No 3 International Monetary Fund - Finance & Development <www.imf.org/external/pubs/ft/fandd/2012/09/basics.htm>

[2] Refer to Chapter 2.1 on ‘The evolution of money’

[3] Félix Gaffiot, Dictionnaire Illustré Latin-Français, (Hachette 1934)

[4] University of Michigan, ‘Middle English Dictionary’ (rev 2006) <https://quod.lib.umich.edu/cgi/m/mec/med-idx?type=id&id=MED9179&egs=all&egdisplay=open>

[5] From Latin ‘salarium’ meaning salary, stipend, pension whose etymology is derived from ‘salt-money’, the soldier’s allowance for the purchase of salt; definition of ‘salary’ from Encyclopædia Britannica (11th edn, 1911) vol 24, p 60

[6] Financial Action Task Force, ‘Virtual Currencies: Key Definitions and Potential AML/CFT Risks’ (2014) FATF Report, <www.fatf-gafi.org/media/fatf/documents/reports/Virtual-currency-key-definitions-and-potential-aml-cft-risks.pdf> accessed 26 June 2018

[7] Blockchain Policy Initiative, ‘Blockchain Policy Initiative Report – Tokens as a Novel Asset Class’ (2017) <https://blockchainpolicy.org/report>

[8] European Central Bank, ‘Virtual Currency Schemes - a further analysis’ (2015) <www.ecb.europa.eu/pub/pdf/other/virtualcurrencyschemesen.pdf>

[9] European Banking Authority, ‘EBA Opinion on “virtual currencies”’ [2014] EBA/Op/2014/08/11/19 <www.eba.europa.eu/documents/10180/657547/EBA-Op-2014-08+Opinion+on+Virtual+Currencies.pdf>

[10] Bank of England, ‘The economics of digital currencies’ (2014 Q3) <www.bankofengland.co.uk/-/media/boe/files/digital-currencies/the-economics-of-digital-currencies>

[11] Pavel Kravchenko, ‘Know Your Tokens: Not All Crypto Assets Are Created Equal’ (Coindesk, 14 August 2017) <www.coindesk.com/what-is-token-really-not-all-crypto-assets-created-equal/>

[12] HMRC, ‘Bitcoin and other cryptocurrencies’, (2014) Policy Paper - Revenue and Customs Brief 9 <www.gov.uk/government/publications/revenue-and-customs-brief-9-2014-bitcoin-and-other-cryptocurrencies/revenue-and-customs-brief-9-2014-bitcoin-and-other-cryptocurrencies>

[13] Jamie Burke, ‘The Next Stage in ICOs: The Community Token Economy’ (Medium, 3 September 2017) <https://medium.com/outlier-ventures-io/the-next-stage-in-icos-the-community-token-economy-cte-995cfb043136>

[14] Gibraltar Financial Services Commission, ‘Statement on Initial Coin Offerings’ (22 September 2017)

[15] Refer to Chapter 1.3.2 (a), particularly Case C-97/90 Hansgeorg Lennartz v Finanzamt München III [1991] CJEU I-03795

[16] ACCA Global – Technical resources, ‘Badges of Trade’ (2011) <www.accaglobal.com/gb/en/technical-activities/technical-resources-search/2011/august/badges-of-trade.html>

[17] HMRC, ‘Business Income Manual: Meaning of trade: badges of trade: summary’, (rev 2017) BIM20205 <www.gov.uk/hmrc-internal-manuals/business-income-manual/bim20205>

[18] Financial Market Supervisory Authority, ‘Regulatory treatment of initial coin offerings’ (29 September 2017) FINMA Guidance 04/2017

[19] Nejc Novak, ‘A call for legal, ethical and sustainable token offerings’ (Medium, 27 June 2017) <https://medium.com/@nejcnovaklaw/a-call-for-legal-ethical-and-sustainable-token-offerings-4d7cd16c64ac>

[20] Refer to Chapter 2, particularly Hedqvist (n 40)

[21] Council Directive 2006/112/EC on the common system of value added tax [2016] OJ L 347/1 (the ‘VAT Directive’), art 135(1)(e)

[22] William Mougayar, ‘Tokenomics - A Business Guide to Token Usage, Utility and Value’, (Medium, 10 June 2017) <https://medium.com/@wmougayar/tokenomics-a-business-guide-to-token-usage-utility-and-value-b19242053416>

[23] ‘Some coins or tokens serve to access or purchase a service or product that the issuer develops using the proceeds of the ICO. Others provide voting rights or a share in the future revenues of the issuing venture. Some have no tangible value. Some coins or tokens are traded and/or may be exchanged for traditional or virtual currencies at specialised coin exchanges after issuance’; European Securities and Markets Authority, 'ESMA highlights ICO risks for investors and firms' (13 November 2017) ESMA50-157-829 <www.esma.europa.eu/press-news/esma-news/esma-highlights-ico-risks-investors-and-firms>