Scope of Application

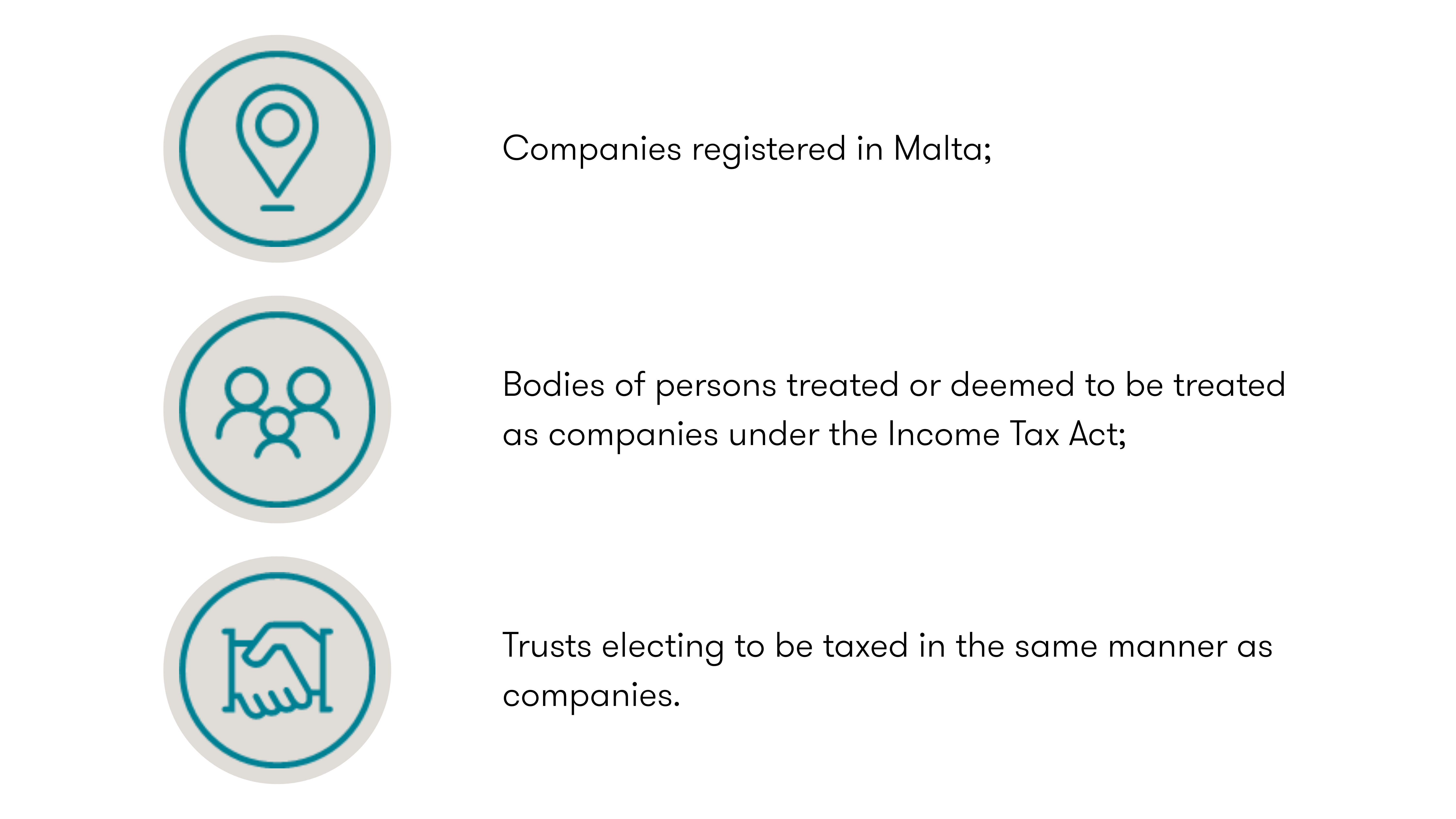

The option is open to:

Any entity may elect for the new regime in respect of chargeable income derived in the fiscal year preceding the year of assessment 2025 (i.e. basis year 2024) and subsequent years.

The Elective Regime

- Final 15% Income Tax

Entities may elect to be subject to a flat 15% tax on chargeable income. This tax is final; it is not creditable, not refundable, and not available as an offset at shareholder level.

- Exclusions

The elective final tax does not apply to:

-

- Dividends received from profits that are not allocated to the Final Tax Account of another Maltese company; and

- Income already taxed at a final rate under other provisions of the Income Tax Act and allocated to the Final Tax Account.

- Five-year Period

Once an entity elects for the 15% regime, it must remain under this system for at least five consecutive years. Should it revert to the ordinary imputation system, it must remain there for a minimum of five years before re-electing for the final tax regime.

- Safeguard Rule

The Regulations include a "higher of" test: the tax payable under the 15% final tax regime cannot be less than the effective tax that would have been payable under the ordinary system, after accounting for refunds available to shareholders under Article 48 of the Income Tax Management Act.

- Final Tax Account Allocation

Profits taxed under this regime are mandatorily allocated to the entity's Final Tax Account.

Policy Context

The introduction of a final 15% tax regime comes at a time when global tax reform is in flux, most notably, following a G7 agreement that now allows the U.S. tax system to operate in a side-by-side manner with Pillar Two. Malta's framework has historically relied on the full imputation system, which effectively eliminated double taxation at shareholder level.

By offering an alternative final tax of 15%, Malta seeks to provide greater clarity and alignment with international tax developments, while preserving flexibility for taxpayers. The regime is elective, allowing groups to assess whether the traditional imputation model or the new 15% final tax provides a more efficient outcome in light of their global tax profile.

What this means for businesses

Entities now face a strategic choice:

- Continue operating under Malta's full imputation system, with its higher headline rate and shareholder refund mechanism; or

- Elect into the 15% final tax regime, accepting the lock-in period and the finality of the tax, while potentially achieving greater international alignment and simplification.

How Grant Thornton can help

Grant Thornton Malta can assist entities in evaluating the potential benefits and implications of electing into the Final Income Tax Without Imputation regime, including:

- Comparative modelling of tax liabilities under both regimes

- Impact analysis in the context of Pillar Two requirements

- Advisory support on elections, notifications, and compliance with the Commissioner for Tax and Customs

For tailored advice on how these Regulations may affect your business, reach out to our Tax team today. We're ready to help you turn complexity into clarity!

-

Luke Aquilina Throughout his career, Luke has been involved in managing a team and providing tax assistance to a portfolio of local and international clients. He has experience in the preparation of tax assessment, consultancy and other compliance services. With the introduction of the local transfer pricing rules, he has been recently involved in certain high-level transfer pricing engagements. Luke has also lectured with different academies on both taxation and transfer pricing.

Luke Aquilina Throughout his career, Luke has been involved in managing a team and providing tax assistance to a portfolio of local and international clients. He has experience in the preparation of tax assessment, consultancy and other compliance services. With the introduction of the local transfer pricing rules, he has been recently involved in certain high-level transfer pricing engagements. Luke has also lectured with different academies on both taxation and transfer pricing.View Profile -

Michael Agius With expertise spanning tax assessment, planning, and consultancy services, as well as Value Added Tax compliance, expatriate and personal tax services, and cross-border due diligence, Michael ensures his clients' financial success across borders. Michael is the go-to expert for navigating the complexities of today's tax landscape with precision and confidence.

Michael Agius With expertise spanning tax assessment, planning, and consultancy services, as well as Value Added Tax compliance, expatriate and personal tax services, and cross-border due diligence, Michael ensures his clients' financial success across borders. Michael is the go-to expert for navigating the complexities of today's tax landscape with precision and confidence.View Profile

Wayne Pisani

Michael Agius