The digitally connected consumer and the challenges for the financial services industry

12 Jun 2019The following speech was delivered by Wayne Pisani, Grant Thornton Partner for Financial Services and Finance Malta Governor, during Finance Malta's 12th Annual Conference, which took place on the 5th and 6th of June 2019 in Malta.

Distinguished guests, in order for Malta to affirm its position as a platform for innovation, all stakeholders are to have a common vision, pursuing an aligned strategy. All regulators, politicians, industry players (old and new), consumers and customer advocates, as well as academics and other influential thinkers gathered at today’s forum possibly concur that the financial services landscape has changed drastically, and has become ever more complicated and subjected to regulation, primarily intended to safeguard the consumer.

But how did we (or the financial services industry) get here? Is this what the consumer is after?

Within the FinTech space we often come across the concept of Software as a Service (SaaS). Mulling over this, I could not help but reflect on … When did finance start being offered as a service? That is – Finance as a Service

Finance as a service

Looking through the ages, the underlying principle has always quite simply been that the industry is expected to facilitate the service of exchange of value, be it by way of procuring daily requirements (a more convenient solution to barter), storing of value as a saving or speculative investment whilst maintaining liquidity, a hedge against risk, or to facilitate other forms of commercial transactions.

The original coin facilitated barter by adding a standardised unit of account, store of value and medium of exchange in the form of coins minted out of minerals, worth their weight, recognised as such in any community. On the other hand, the evolution of money into bank notes, taking the shape of receipts of value issued by the institution holding the valuables against which the bank notes or receipts are issued, led to the first complication … paper notes recognised in one community would not necessarily be recognised or accepted as a store of value by other communities. Think of trying to present a 15th century Medici note as a store of value on the eastern side of the Silk Road.

Nations developed their own currencies for their communities; standard exchange rates were needed; standards had to be developed and rules and regulations took over the space.

Is such a system, originating from servicing micro-communities, capable of servicing today’s global economy? The latest technology has repeatedly been applied to facilitate such transfer of value. In 1871 Western Union resorted to telegram communications to facilitate the transfer of money in dematerialised format, launching the first form of e-money.

The fact, however, remains that multiple currencies, multiple banks, and multiple intermediaries have led to multiple rules and regulations.

Reverse engineering the problems we are facing might not be an efficient way to overcome the complexities of what is perceived as an overregulated industry. Look at the origins and apply today’s technology to the original problem. We live in a digitally connected world which evolved from telegram in the 19th century to internet-enabled things requiring little or no human intervention. The consumer wants to be in the driving seat but has gotten used to being pampered and having the peace of mind of a safe financial environment. What should therefore the financial services practitioners’ vision focus on? When we think of setting a vision, we might instinctively think of a telescope and long eyesight… but what about what is right in front of our eyes/under our noses? Why can’t the consumer have Bitcoin functionality with e-money? Similarly, robo-advisory is practical and convenient … but are the consumers trusting the same?

People will always need financial services

Be it an in-store purchase using a chip card, an online purchase clicking at your keyboard or a mobile purchase using your augmented reality glasses, people will always need financial services to transact the most basic of financial transactions a mere exchange of value in the form of a payment, let alone investment and insurance products. Hence, the good news (at least for those in the industry) is broad agreement that financial services will continue to be of fundamental importance to society and a part of daily life.

Nonetheless, there is distrust in the industry in an age when trust is moving away from institutions to individuals. The Edelman TRUST BAROMETER, an annual global trust survey, now in its 19th year, which measures attitudes about the state of trust in business, government, NGOs and the media, surveys over 33,000 respondents from 27 different countries. The data in this study is in line with what I, and probably many of you, experience in communication with clients.

Although trust in the industry rose by 8 points over the past five years, the numbers show that nearly half of the mass population surveyed believe that the system is failing them. In conjunction with pessimism and worry, there is a growing move towards engagement and action as a consequence to news reports. But people are encountering roadblocks in their quest for facts, with the 2019 Edelman Trust Barometer reporting that 73 percent are worried about fake news being used as a weapon.

The industry needs to re-imagine itself if it is going to be trusted and thriving going forward.

Understanding the needs of the digitally connected consumer

Getting to know our clients is not just about due diligence but it is also about understanding their business and their requirements. The financial services industry needs to focus on the fact that we live in a digitally connected world. The consumers’ expectation of a financial service is underpinned by the need to facilitate their daily requirements, be it payments, monitoring of one’s finances or performance of one’s investments.

Let us not forget that whilst more than two-thirds of the adult population has access to banking and mobile money accounts, according to the 2017 Global Findex high-level statistics based on nationally representative surveys of more than 150,000 adults in over 140 economies, 1.7 billion adults remain unbanked.

Despite the divergence in trust, there seems to be an urgent desire for change. Only one in five feels that the system is working for them. Technology may help to bridge the gap. This is however to happen within a secure environment where regulators and the financial services players strike the right balance between safeguarding the consumer and facilitating the digitally connected experience. Professionalism - competence, care and ethics - are the cornerstone of rebuilding trust. While it is important to have clear values and a social purpose, both at industry and practitioners’ level, ethics and culture cannot be externally imposed (e.g. by regulators). Industry must drive change. Being responsible and accountable, from board through to the front line, and right across the entire supply chain.

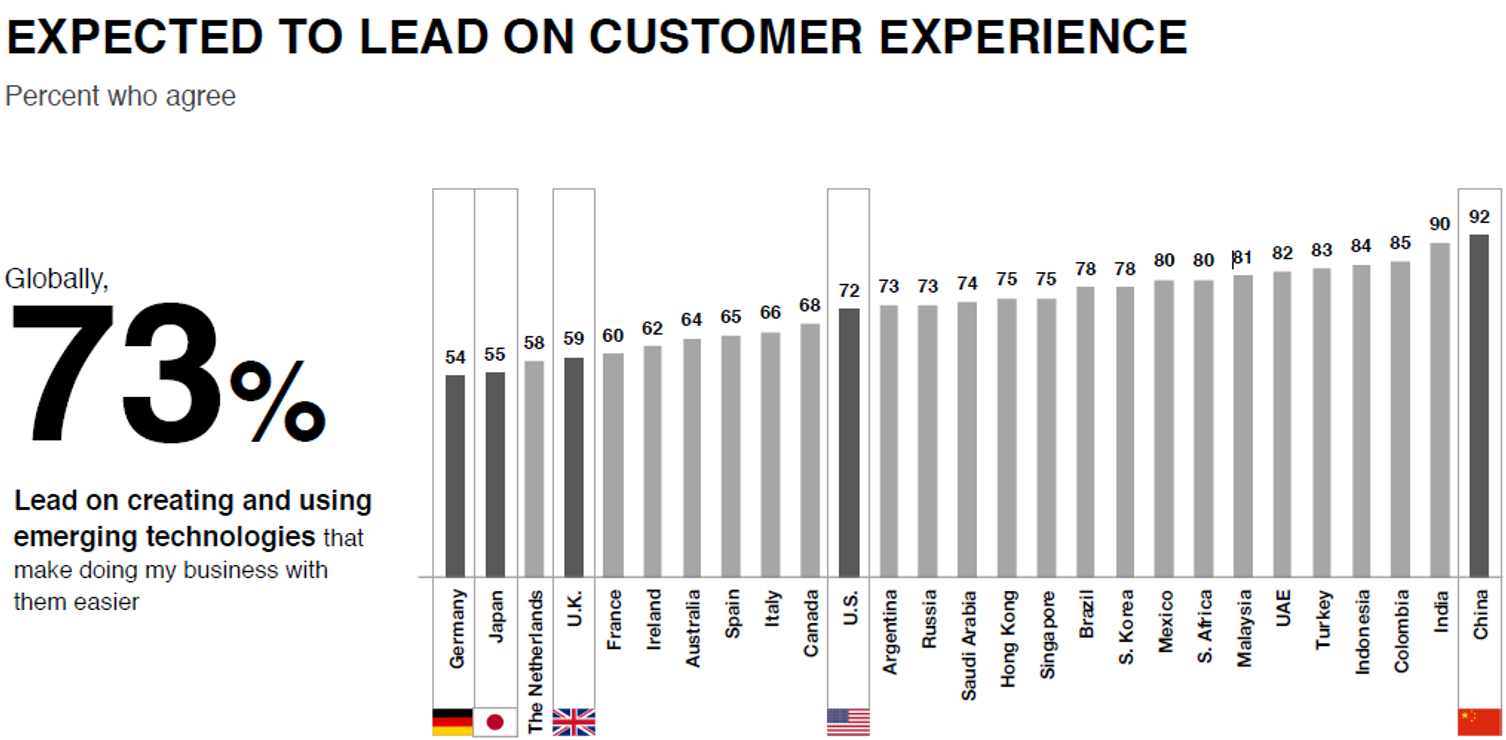

The financial services industry has moved rapidly to innovate, as digital insurgents threaten to take market share from incumbent brands. In light of the growing divergence in trust between publics, it is important to recognize two equally important roles of innovation:

- 73 percent believe it is important for financial services to lead on creating and using emerging technologies that make doing business with them easier;

- 70 percent believe it is important for financial services to lead on social issues that make the world a better place for everyone.

Globally, the most important social issue for financial services companies to address is income inequality and financial security. Yet, the innovations designed to broaden access and help close the gap are lagging far behind traditional products and services in terms of trust.

Looking at examples from the last decade, one could think of the M-Pesa model adopted in some African countries: a service which would allow microfinance to borrowers who would conveniently receive and repay loans using mobile airtime, an alternative form of extending credit. Similarly, with Bitcoin, a protocol intended to disrupt the payment process by introducing a distributed network of transaction verification.

Whilst these may have served some communities, widespread adoption is still somewhat lacking with trust in these solutions lacking behind traditional banking, insurance and credit card services. As the industry continues its digital transformation, customer experience with an emphasis on integration is critical: the most useful innovation when it comes to choosing a financial services company seems to be a platform that integrates all aspects of a customer’s financial life, selected by 53 percent of respondents in the Edelman study.

However, the recurring important innovations for financial services companies to help make the system work for everyone should focus on:

- Protecting data and assets

- Fairer access to credit

- Financial inclusion for the un- and under-banked; and

- Digital gamification to advance financial literacy

There seems to be a dire need for any such innovation to be underpinned by a regulatory framework which balances the need for consumer protection with the scalability to adapt to innovative approaches.

The industry is possibly drowning in rules. Despite this, trust seems to follow regulated business (consider the banks in the afore-cited trust barometer chart).

Regulation and clarity are key, as is the case of the framework promulgated by the Maltese Government to regulate the DLT and innovative technology arrangement space, as technology agnostic as possible to maintain regulation in touch with innovative developments.

Various developments are in the offing as are the numerous projects spearheaded by the Government of Malta in the innovation sector which Hon Silvio Schembri will surely share with us later today as well as the MFSA’s Vision 2021 and the FinTech Strategy introducing 6 key pillars focusing on regulation (including a regulatory sandbox), the facilitation of an ecosystem including an innovation hub, an open architecture enabler, international links, knowledge and education (including R&D) and above all a focus on cybersecurity, aspects which the MFSA’s CEO Mr Joseph Cuschieri will elaborate upon in his address.

New regulations and planned reforms to fine tune the traditional financial services pillars are also under way, constantly improving on Malta’s evolved regulatory framework which is now in its third decade, as well as a number of consultations on applying innovative technologies to financial services as is the case with security token offerings (STOs). The list could go on.

On the other hand, a new dynamic in the form of self-regulation is also emerging, possibly more nimble than the regulators to keep the financial industry in check. … As seen in the crypto dynamics over the past year, with fund raising initiatives shifting from ICOs to exchange driven issues of tokens and the coining of the term IEO – Initial Exchange Offering (as opposed to ICO), this can be construed as evidence that self-regulation has more trust than government driven regulation, and that self-generating ethical culture is more successful at engendering desirable behaviour than externally imposed rules.

It is also pertinent to appreciate that the more we regulate, the more unbankable the unbanked become. In an effort to secure the systems, the ever-increasingly onerous requirements are lifting the bottom rung of the ladder further off the ground. The regulation might be well-intentioned, but it should not be the prerogative of an exclusive community.

Within this reality, cognitive enterprise should identify the resources available and adopt the best-suited technologies to implement its strategy. Data is key.

The benefits (and necessity) of harnessing the tidal wave of data brought about by digitisation and interconnectivity can help industry better understand and meet the needs of individual customers, can fine tune insurance pricing and signal to customers how they need to better manage risks, and when harnessed correctly prevent problems.

The data economy could be as big as financial services within the next five years. But, more voluminous and more granular digital data brings heightened risk of cybersecurity, privacy and data breaches. The need for Boards to ask astute questions to challenge management when it comes to data or technology driven proposals is crucial.

Other risks may include the potential for unintended adverse outcomes, such as the avoidance of health checks for fear an insurer would be able to access information and deny cover, or implicit and explicit bias in decision making systems based on data. Having more data might also lead to “choice overload”, confusion and information fatigue. In open data systems, customers could quickly lose track of the data disclosed and what consents had been given.

The need to understand and cater to customer needs

Customers are becoming increasingly demanding: they want personalised, flexible and frictionless financial services, delivered on digital platforms, anytime and anywhere. Millennials in particular are demanding greater personalisation and digitisation, with a focus on the experience. How the industry interacts with those at the other end of the spectrum, retirees and superannuants, is another focus area for an all-inclusive financial services vision going forward.

Intensifying consumer expectations around a firm’s corporate social responsibility record and ways to not only innovate, personalise, and modernise products and services but also be transparent about its operations, is another reality. Information and disclosure need to work in a digital environment and be both simple and useful to meaningfully engage customers: if customers don’t engage, they won’t understand, and they will not make good decisions.

Within this context, recently I was asked whether I perceive crypto to be a threat to established financial institutions. Crypto might not be a threat to the institutions, if the industry embraces change and harnesses the power of innovation. Case in point is JP Morgan’s move to launch the JPM Coin, intended for the bank's wholesale payments business that daily moves $6 trillion around the world.

I would however advocate for incumbent financial institutions to look beyond crypto and be less focussed on the FinTech or incumbent dichotomy, and watch out for competition from the tech and ecommerce giants like Google, Apple, Facebook, Amazon and Alibaba since they have the power of aggregated communities; possibly a precursor to open banking and open data regimes.

Case in point is PayPal’s 11th position on this chart for what started as a technology service in the form of a digital wallet in the late 1990s.

Customer expectations and demands are set by the tech and ecommerce giants: people are now expecting their financial services experience to be like their experience with Uber or Amazon.

Truthfully, this comes at the cost of their insidiously mining data about us and our choices, preferences, social status and purchasing options (which therefore also includes purchasing power). This data puts them in a prime position to pre-empt customers’ wants and wishes and, at the same time, are in a position to selectively engineer the user’s online social environment, making the user’s choices feel far more like choices than they effectively are.

In addition, in the “war for talent”, much needed data scientists and engineers seem to be choosing the more flexible work environments within tech companies as Google over a bank or established financial institution. Aside from the fact that banks are part of the establishment, they are also resistant to change. Why would anyone with a smattering of inventiveness and creativity choose to work in an environment which relentlessly works to maintain the status quo, when other outfits are supporting the creative leash and letting them run with ideas, even if the ideas eventually go nowhere? Being allowed to fail is the ultimate unleashing of creativity.

In the end it’s all about people

Finance is not an end in itself but exists to serve people. The ultimate objective of strengthening competition and for open data regimes is to get better outcomes for people; that millennials trust individuals not institutions; that establishing the trustworthiness of people will rebuild trust in the industry; that focusing on the demand side and “the power of personalisation” are key to maintaining relevance in today’s online interconnected and digital world.

So what can we conclude as the broad vision of the future? The industry will be more professional, ethical, trustworthy, socially responsible and accountable; reflective of, and responsive to, diversity; guided by the needs of “real people” when making decisions; transparent, open and interconnected; savvy about, and enabled by, data and technology.

All individuals in the industry, regulators and advisers, have a role in making sure this vision is realised.

And what about Malta? Malta will need to continue building on the scalability of its value offering, providing a euro Mediterranean platform for innovation to facilitate the drive for digital connectivity.